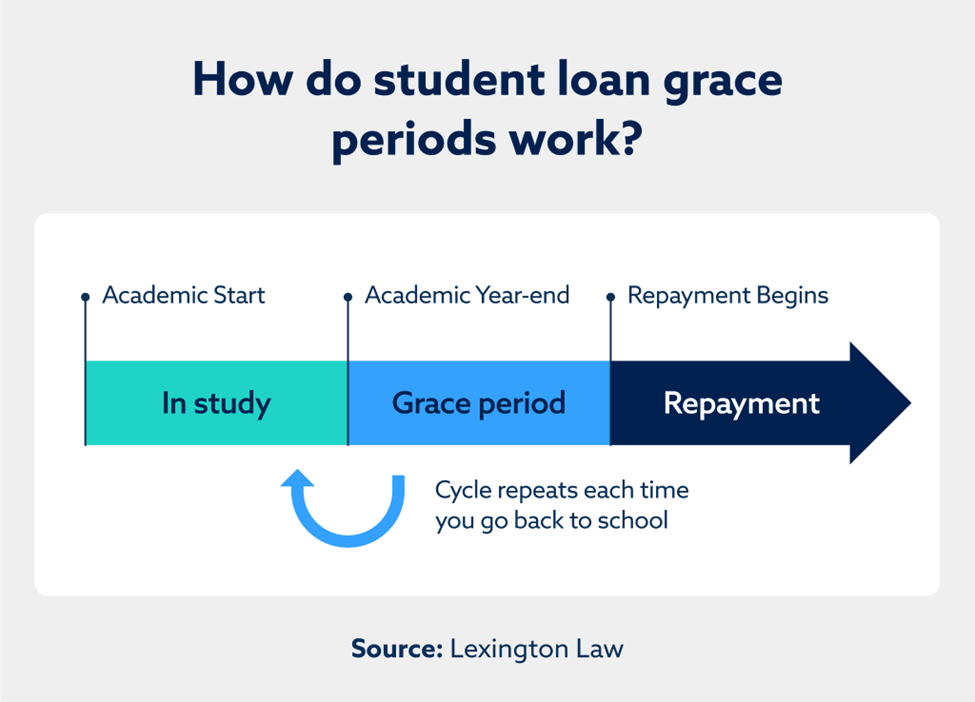

A student loan grace period is a set amount of time granted to students before they must pay down their loans. Grace period terms vary based on loan types.

The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

A student loan grace period is a set amount of time granted to students before they must pay down their loans. Grace period terms vary based on loan types, and some student loans don’t have grace periods at all.

The average student loan debt in 2022 was $37,104 per borrower, which helps reinforce why grace periods are so important to recent graduates. Learning how grace periods work—and whether they can be extended—can help students be more prepared for life after graduation.

Key takeaways

- Federal student loans usually have a six-month grace period.

- A student loan grace period can be extended under certain circumstances, such as military service.

- You may be eligible for student loan forgiveness later on in your career.

Table of contents:

- How long is my student loan grace period, and when does it start?

- Can my grace period change?

- What happens when the grace period ends?

- Can I make payments during the student loan grace period?

- How do student loans affect credit?

- Capitalize on your student loan grace period with Lexington Law Firm

How long is my student loan grace period, and when does it start?

Most student loans have a grace period of six months. Here’s the breakdown:

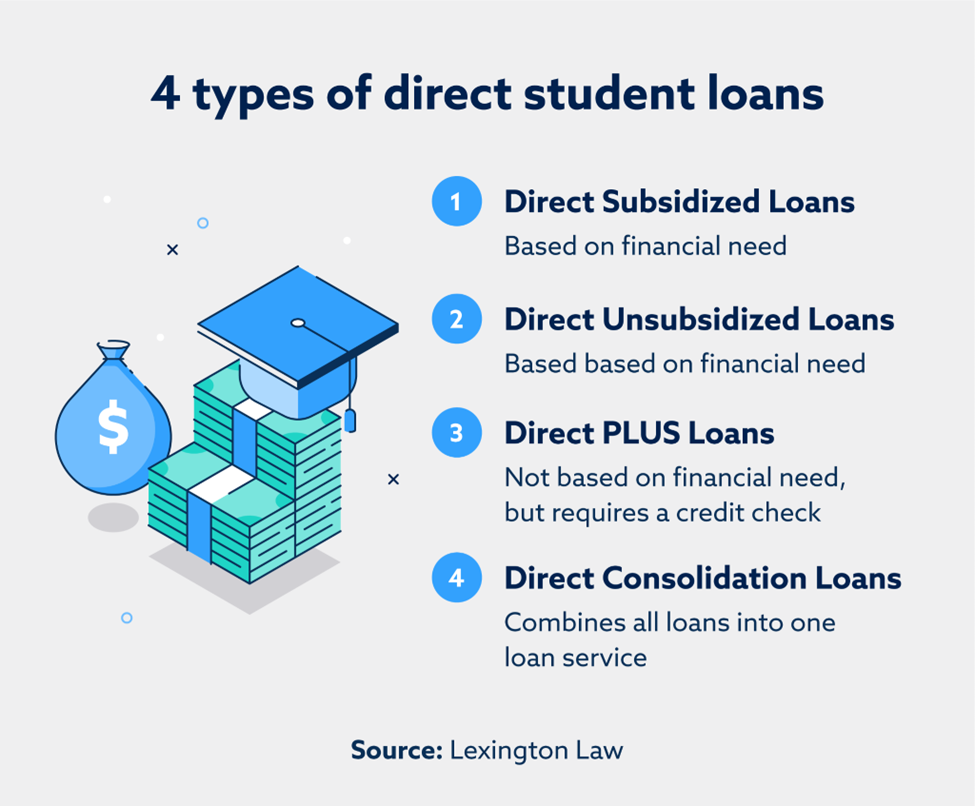

- Federal direct subsidized loans and direct unsubsidized loans: Six months

- Federal Stafford subsidized and unsubsidized loans: Six months

- Federal PLUS loans: Six months (parents of students may need to request the six-month grace period on the loan application)

- Federal Perkins loans: Nine months

- Private loans: Grace periods vary by the lender. Many private student loans offer a six-month grace period, but some require repayment as soon as the loan is disbursed. The loan agreement should state when payments are due.

For most loans, including federal student loans and the majority of private student loans, the grace period starts as soon as a student drops below half-time enrollment. This means dropping enough classes, taking a gap year or graduating are all situations that can trigger the start of your grace period.

The definition of “half-enrollment” varies at each institution, so make sure you check with your school and understand the threshold.

Can my grace period change?

Yes, your student loan grace period can change, either by being cut short or by restarting. Similar to a credit card grace period, some factors that can affect your student loan include:

- Active military duty: If you’re called to active military duty for more than 30 days before your grace period officially ends, your six-month grace period will restart when you are discharged from service.

- Consolidating your loans: Consolidation can forfeit/cancel out whatever time remains on your student loan grace periods. You can also wait to consolidate until the end of your grace period to take full advantage of the payment-free time on hand.

- Re-enrolling in school: Re-enrolling in school with a half-time course load or more before your grace period ends will effectively extend your grace period. Should you drop below half-time enrollment (via withdrawing, dropping classes or graduating), you’ll be given a six-month grace period.

What happens when the grace period ends?

Before your grace period ends, you should receive a repayment schedule from your loan servicer that details how much your payments are and when they’re due.

For those wondering who to contact for questions about repayment plans, we recommend contacting your loan servicer. They can help you request a different repayment plan (such as income-driven repayment plans) and learn what other options you have for repayment (such as loan consolidation, deferment and forbearance). These requests often take months to approve, so contact your loan provider as soon as possible.

Concerning repayment plans, it’s perfectly fine to contact your provider if you feel that you can’t afford the initial proposed payment schedule. It’s ultimately better to change the repayment plan than payments in the future.

Can I make payments during the student loan grace period?

Yes, and you can even make payments while you’re still in school. Early payments are a great way to help you pay off your loan sooner and graduate with a smaller loan and less stress. If you can’t afford full payments, covering the cost of interest is another great way to help you pay off your student loans faster.

If you’re wondering what increases your total loan balance, you should know that unpaid interest can potentially cause a debt to balloon over time. You should receive a letter or email from your loan provider reminding you that you can pay off your interest before it’s added to your balance or capitalized.

How do student loans affect credit?

Student loans can affect credit both positively and negatively, just like all loans. For example, consistently making timely payments on your loan can cause your credit to improve over time. However, if you miss or make late payments, you’ll see a drop in your credit due to a negative payment history.

A student loan going into default can also drastically impact your credit. Default happens if you miss at least nine months of payments, which will prompt creditors to add this as a derogatory mark on your credit reports. This negative item can stay on your reports for up to seven years, possibly moving you closer to a bad credit score and impacting your ability to be approved for future credit.

Note that your loan going into default doesn’t mean you can ignore your payments. If you do, loan providers can take action against you, resulting in wage garnishment, withholding tax refunds and applying additional loan fees or interest accruals.

If you can’t make your loan payments anymore, reach out to your loan provider to understand your options.

Capitalize on your student loan grace period with Lexington Law Firm

As you repay your student loans, you must watch your credit reports to make sure everything is reported accurately. Even one misreported late or missed payment can significantly impact your credit. If you’re unsure where to start with credit report errors, let the team at Lexington Law Firm help. We can offer you a free credit report assessment to help get you started.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.