The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

Declaring bankruptcy doesn’t eliminate all debts. Some debts a bankruptcy won’t discharge include tax debt, child support, alimony and court-ordered fines and fees.

The U.S. Courts reported that bankruptcies fell nearly 12 percent in 2022 compared to the previous year, but there were still nearly 400,000 filings overall. Only 13,125 of these were business bankruptcies, which means that hundreds of thousands of Americans are still filing for bankruptcy each year. Bankruptcy can help you manage or even eliminate debts, but do you get out of all debts if you declare bankruptcy?

Here, you’ll learn what bankruptcy can and can’t do as well as the pros and cons of filing. By understanding the ins and outs of bankruptcy, you’ll have a better idea of if it’s the right choice for you or if you should seek an alternative method of taking care of your debt.

What happens when you file for bankruptcy?

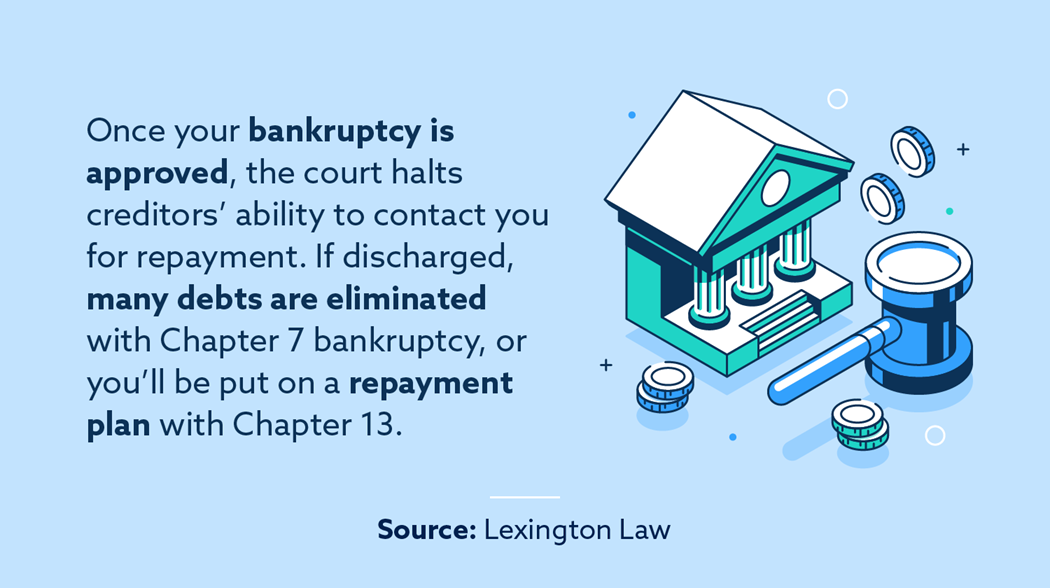

When you file for bankruptcy, you’re petitioning the court to begin the process of eliminating your debt or getting on a repayment plan. Once filed, there are additional steps you must take to get approved for your bankruptcy. If the bankruptcy is approved and all goes to plan, you’ll receive a discharge. Otherwise, you’ll receive a denial, which is also known as a dismissal.

The most common forms of bankruptcy for individuals are Chapter 7 and Chapter 13. Each one offers unique benefits as well as disadvantages. But whether you file for Chapter 7 or Chapter 13, the bankruptcy filing process is similar. Here’s a brief overview of the steps to file for bankruptcy from start to discharge:

- Meet with an attorney if possible.

- File with the court.

- Organize your financial information.

- Meet with a bankruptcy trustee.

- Take mandatory debt counseling courses.

- Receive a discharge or dismissal.

Chapter 7 vs. Chapter 13 bankruptcy

The primary difference between Chapter 7 and Chapter 13 bankruptcies is that Chapter 7 eliminates debts and Chapter 13 puts you on a repayment plan.

Chapter 7 bankruptcy is also known as a “liquidation” bankruptcy because it’s the most common option for eliminating most of your debt. During the Chapter 7 bankruptcy process, you meet with a trustee who will review all of your assets and decide which assets need to be sold to pay back creditors.

Some of your assets may be exempt from being sold during a bankruptcy—these nonexempt items will vary from state to state. Once the assets are liquidated to repay creditors, many of the remaining debts will be eliminated once discharged.

Chapter 13 bankruptcy puts you on a repayment schedule with your creditors. When you meet with a trustee during the Chapter 13 process, you’ll submit a proposal for a repayment plan based on your income, expenses and other financial circumstances. If approved, you’ll repay your creditors over the next three to five years before the bankruptcy is discharged.

Both bankruptcy types stay on your credit report, but Chapter 13 stays on your report for only seven years, while Chapter 7 stays for 10 years before the bankruptcy is removed.

Do you get out of all debts if you declare bankruptcy?

Neither kind of bankruptcy will eliminate all your debts. Bankruptcy doesn’t eliminate secured liens or prevent repossessions of property. A discharged bankruptcy also doesn’t cover court-ordered fines or fees, tax debts, alimony or child support.

What debts are never discharged by bankruptcy?

Simply put, debts that aren’t discharged by a bankruptcy are usually debts owed to the government or to the courts.

In addition to the debts covered in the previous section, bankruptcy won’t eliminate:

- Many student loans

- Debts owed for personal injury or death as ruled by a court

- Fines and penalties from the court, like traffic tickets or criminal restitution

Difficult debts to discharge with bankruptcy

While student loans and tax debts aren’t typically covered in a bankruptcy, it’s sometimes possible to have the debts reduced or eliminated. These debts can be difficult to discharge, but there are circumstances that may help you qualify.

If you can prove that you’re unable to maintain a minimal standard of living due to financial hardships, you may qualify for the elimination of student loan debt. For those who don’t qualify, it may be a better option to contact the loan provider to negotiate a restructuring of the loan and repayment plan.

The courts don’t usually assist with discharging income tax debt unless there are special circumstances. Fortunately, the IRS offers a few options for those who qualify. On the IRS website, they provide applications for programs like Offer in Compromise, but one of the qualification standards is not currently being in a bankruptcy proceeding.

What bankruptcy can do

Both Chapter 7 and Chapter 13 bankruptcy offer relief for those who are struggling to repay their debts. Understanding exactly what bankruptcy can do can help you decide if it’s the right option for you.

Stop collection calls

Once your bankruptcy filing is filed with the bankruptcy court, an automatic stay goes into effect, preventing creditors and collectors for taking any action against the debtor(s). They’ll contact all of your creditors and collection agencies to let them know you have filed for bankruptcy, which will prevent them from contacting you for repayment.

Temporarily stop foreclosures and repossessions

If a foreclosure, repossession or eviction is still pending, the automatic stay puts a hold on these actions as well. For those who file Chapter 7, the process may delay the foreclosure or repossession, but it’s possible your assets will still be seized as part of the liquidation process, or the creditor could seek relief from the automatic stay from the court, if they have grounds to do so. If you file Chapter 13, you’ll be put on a repayment plan.

Renters in the process of eviction may delay or completely halt the process once the bankruptcy is filed . However, attorney Curtis Lee with Upsolve warns renters that some states don’t allow them to stay in the residence while catching up on past-due rent.

Eliminate unsecured debts

Chapter 7 bankruptcy can help by eliminating unsecured debts, which includes:

- Credit card debt

- Medical bills

- Utility bills

- Personal loans

With Chapter 13, these unsecured debts become part of your repayment plan.

Eliminate secured debts

Although bankruptcy can help eliminate secured debts, you’ll need to give up the property. This means that if you have secured loans in the form of a car or a home, they’ll be repossessed by the bank but you won’t be responsible for the outstanding debt.

What bankruptcy cannot do

As you’ve learned, bankruptcy doesn’t get you out of all your debts and responsibilities. Next, we’ll discuss what bankruptcy can’t do so you can set your expectations accordingly.

Stop property seizures

Bankruptcy can eliminate the debt owed on secured loans for which you provided collateral, but it doesn’t eliminate the secured lien or stop the repossession of those properties. You may also be required to give other nonexempt assets to the trustee for sale in order to pay back creditors when filing Chapter 7.

Stop court-ordered payments or tax debts

If you owe child support, alimony or other court-ordered payments, the debts will not be eliminated through a bankruptcy discharge. You’ll also still be responsible for any tax debts unless you’re able to negotiate with the IRS or qualify for one of their programs. (Note: certain taxes over three years old may possibly be discharged under special, defined circumstances.)

Eliminate student loans

Unless you qualify due to special circumstances, student loan debt won’t be eliminated when filing for bankruptcy. To qualify for student loan debt elimination, you’ll need to prove undue hardship, which has a high standard for qualification.

Eliminate fraudulent debts

In some cases, people defraud creditors by lying on credit applications, and these debts won’t be discharged if the creditor files an adversary proceeding (lawsuit within the bankruptcy.). For example, if you qualified for a loan by saying you make $500,000 per year but really only make $60,000, that would be a fraudulent debt.

Alternatives to filing for bankruptcy

Not only is there no guarantee that debts will be eliminated when filing for bankruptcy, but the bankruptcy can also stay on your credit report for seven to 10 years. Before filing, it may be helpful to know that there are alternatives to filing for bankruptcy.

- Find additional income: Rather than filing for bankruptcy, some people try to get extra hours at work or find work they can do on the side to pay down their debts.

- Reduce your monthly spending: When you create a budget, you’re able to use the money you save to pay down your debts.

- Ask friends and family for a loan: One reason many people get buried in debt is due to interest, so a loan from a friend or family member relieves you of high-interest payments while you pay off your debt.

- Sell personal assets: Rather than selling your assets through a bankruptcy and damaging your credit, you can sell assets on your own (instead of filing bankruptcy) to begin paying down your debts.

- Refinance your mortgage or auto loan: Talk with your lender about refinancing your loan, which may reduce your monthly payments and interest rates.

How to fix your credit after a bankruptcy

If you have to file for bankruptcy, your credit score will be affected for the next seven to 10 years. This can make it difficult to secure new loans and lines of credit. A poor credit score also typically leads to higher interest rates and larger down payments and security deposits. Fortunately, there are proven ways to repair your credit after a bankruptcy.

Lexington Law Firm has a team of credit repair consultants who have experience with helping people repair their credit after filing for bankruptcy. We have services that will allow you to monitor your credit, and our consultants will be there to guide you through the repair process. If you’re looking to repair your credit after a bankruptcy, review our wide range of services or contact us today for more information.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.