The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

Banks, credit unions and online lenders provide debt consolidation loans once borrowers go through the application process and meet certain criteria.

The average American credit card debt is roughly $5,010 per person, and many Americans struggle with additional forms of debt like loans and other bills. Loans come with interest rates, which make the overall cost higher than the original amount borrowed, and past-due bills can harm your credit. Fortunately, debt consolidation loans can help.

Today, you’ll learn what these loans are as well as how to get approved for a debt consolidation loan in five simple steps. Regardless of where your credit stands, you may get approved for one of these loans to help you lower interest rates and save some money as well.

What is a debt consolidation loan?

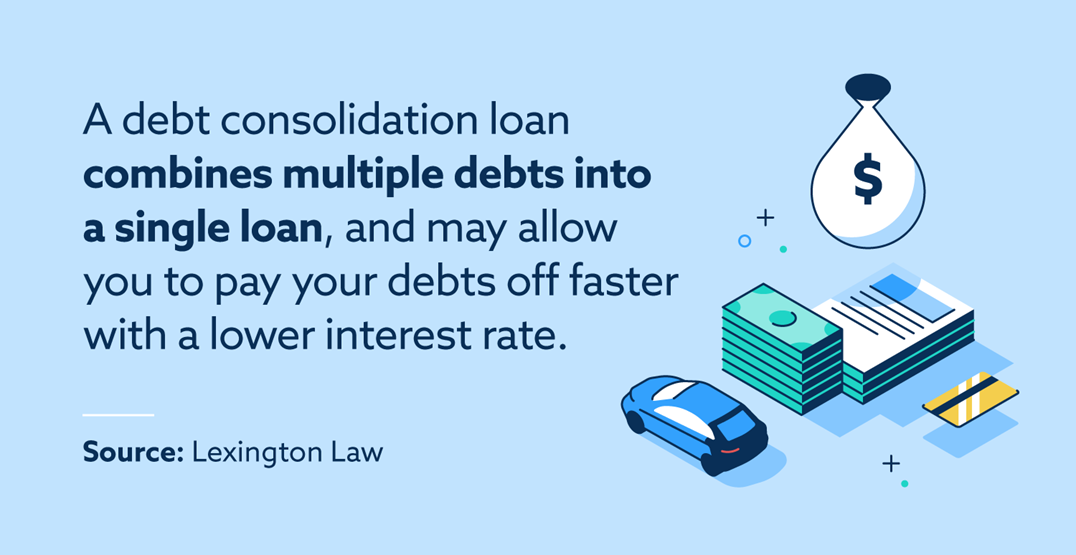

A debt consolidation loan is an unsecured personal loan designed to simplify the debt repayment process. Combining multiple balances into a single fixed-rate loan can potentially allow you to secure a lower interest rate on your debts and may enable you to pay them down faster.

Not only can you use debt consolidation loans to pay off other loans, but many people also use these loans to consolidate their bills. If you’re looking to consolidate credit card debt, you can use a loan or a balance transfer card.

How to apply for a debt consolidation loan

Debt consolidation means combining multiple debts into a single loan with one fixed monthly payment. This type of personal loan will ideally allow you to combine several high-interest debts into a new loan with a lower interest rate. If managed properly, it can yield significant money-saving benefits. However, there are a few steps you should take before applying for a debt consolidation loan.

Step 1: Check your credit

Your credit is one of the primary factors lenders will look at to determine whether or not your loan will be approved. Typically, approval is more likely if you have at least a good FICO credit score, which ranges from 670 to 850.

There are many ways to check your credit score and report for free, and this is often a good idea before you apply for debt consolidation loans. When a lender checks your credit, the hard inquiry can temporarily hurt your credit, so it’s better to know your chances of approval beforehand.

If you have poor credit, here are some ways to improve it before applying for a loan:

- Catch up on late payments that are less than 30 days old

- Pay off smaller debts to reduce your credit utilization rate

- Check your credit report for errors, and challenge any errors you find

Step 2: Make a plan

Before you apply for loans to consolidate your debt or bills, it’s beneficial to make a plan. You can start by listing all of your various debts and bills that you want to pay off. These may include:

- Credit cards

- Bills

- High-interest loans

- Store credit cards

You can then add up each of these debts and the required monthly payments for each of them. Now, you can make a plan to see how much money is needed to pay these debts off and how much money you will save when you get a consolidation loan.

When devising this plan, you may want to create a monthly budget at the same time to ensure you can make the new monthly consolidation loan payments on time.

Step 3: Shop around

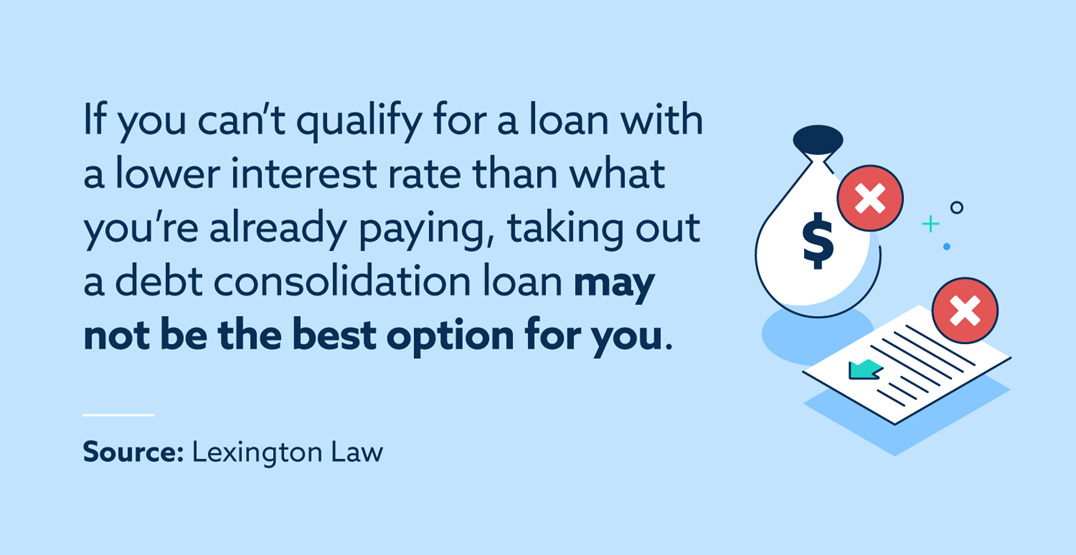

Whenever you’re applying for loans, remember that there may always be a better deal out there. Different lenders provide different interest rates on loans, and the lower the interest rate, the better. You also have different options when it comes to where you go to take out a loan:

- Bank loans: Your current bank may provide loans, and if you have a long-term relationship with the bank, they may be more likely to approve a consolidation loan with bad credit.

- Online lenders: There are many online lenders, and these lenders are known for providing loans to those with bad credit. Keep in mind that lenders who specialize in providing loans to people with bad credit may also have higher interest rates.

- Credit unions: These not-for-profit financial institutions are often local and may provide you with better rates than other options. In order to take out a credit union loan, you’ll need to apply to be a member and meet certain criteria.

Step 4: Go through the application process

Now that you have settled on a financial institution, it’s time to go through the application process. A debt consolidation loan application may require the following documentation:

- Proof of residence

- Bank and other financial statements

- Pay stubs or proof of income

- Government-issued photo ID

After you provide the necessary documentation, the lender will run a hard inquiry to check your credit history and score. Credit scores are a way for lenders to assess the risk level of potential borrowers. Negative marks on a credit report may indicate that a person is likely to default on a loan, which is why it’s helpful to improve your credit score before you apply.

Step 5: Close the consolidation loan and make your payments

If you’re approved for the loan, the lender may provide your funds in one of two ways:

- Paying creditors directly: The lender may pay off your debts directly. If this is the case, it’s recommended to continue making your payments until you receive written verification that the debts are settled.

- Direct payment to the borrower: The lender may pay you directly by depositing the money into your bank account or providing you with a check. If this is the case, you’re then responsible for paying off your creditors. You may want to pay off the creditors sooner rather than later so you don’t continue to accrue interest fees.

What if your debt consolidation loan is denied?

If your loan application is denied, it can be for a variety of reasons. The lender may see something on your credit report that throws up a red flag, or you may not meet their income criteria. Should this happen, you will receive a letter through the mail or email explaining why they denied your application.

A denial of a loan isn’t the end of the road, and you have a few options you can turn to:

- Try to apply for a lower amount: Depending on the amount you request, the lender may decide that you’re too high of a risk. By lowering the amount, they may approve the loan.

- Apply with other lenders: Applying for loans triggers hard inquiries that temporarily lower your score, so do your research beforehand. If you’re denied, look for lenders that offer preapproval or specialize in debt consolidation loans for bad credit.

- Look into debt management plans: There are various companies that offer credit counseling and debt management plans to help you repay your debt. Some of these services require payment for the counseling, but there are also some that are nonprofit organizations.

- Sign up for credit repair: If your loan was denied because of poor credit, it might be due to errors on your credit report. Companies like Lexington Law Firm offer credit repair services and challenge credit reporting errors on your behalf.

Debt consolidation loan FAQ

Here we’ve provided some helpful answers to debt consolidation loan FAQ.

How hard is it to get a debt consolidation loan?

If you have a bad credit score, it can make it difficult to get a debt consolidation loan. You may want to try a bank or credit union that you have a relationship with, or try to repair your credit first.

How can you qualify for a debt consolidation loan?

Typically, a good credit score of 700 or higher is the best way to qualify for a debt consolidation loan. This will also help you get the best interest rates.

Can debt consolidation loans hurt your credit?

The initial hard inquiry into your credit score will temporarily lower your score. As long as you stay current with your monthly payments, your score should be fine and will potentially get higher over time.

What’s the minimum credit score needed to get a consolidation loan?

A fair FICO® credit score of 580 to 669 may be enough to qualify at financial institutions for a debt consolidation loan.

Improve your credit before taking out a debt consolidation loan

As you now know, debt consolidation loans can be a great way to pay off your debt faster and potentially lower your interest rates. If you have poor credit and need assistance before applying for a debt consolidation loan, allow Lexington Law Firm to help.

We have a team of credit professionals, and we’ll assess your credit report to see if any errors are harming your credit. We also offer additional services to help you work toward and maintain good credit. Sign up for your free credit assessment today.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.