The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

Debt forgiveness occurs when a lender forgives either a portion of or the entire debt owed by a borrower from a loan or credit account.

Debt forgiveness occurs when a portion of a loan or the entire remaining amount of a loan or credit line is canceled, relieving the borrower from the obligation of repayment. Before moving forward with debt forgiveness, it’s important to consider the potential benefits and drawbacks so that you’re fully prepared.

It’s also important to note that debt forgiveness differs from debt relief, which involves reorganizing debt to facilitate repayment—but doesn’t cancel the debt.

Continue reading to learn more about debt forgiveness and explore different options that you may qualify for.

Debt forgiveness benefits

Debt forgiveness can provide relief to those who are struggling to make payments, and it has the following benefits:

- You can avoid filing for bankruptcy: Debt forgiveness can prevent the need to file for bankruptcy, which would severely damage your credit for up to seven to 10 years.

- You can pay less than your original obligation: While the amount you’ll pay varies depending on the program you choose, it is typically much less than the amount you originally owed.

- You can pay your debts quicker: Through debt forgiveness, you can significantly reduce your debt in a much shorter time frame than you initially expected.

Debt forgiveness drawbacks

On the other hand, debt forgiveness has the following downsides that you should be aware of:

- You may owe taxes on the amount that’s forgiven: In general, canceled debt is considered taxable income that you may be responsible to cover.

- You could owe more than your original obligation: Many debt relief companies charge excessive fees that could equal or exceed the amount you originally owed. Additionally, it’s important to change your financial habits so you don’t continue to rack up debt.

- Your credit may take a hit: Depending on the type of debt that’s forgiven, you could notice a negative effect on your credit. However, this will likely not be the case if the debt in question is student loans or medical bills.

Because of these drawbacks, you may want to consider other debt management options.

Debt forgiveness vs. debt consolidation

An alternative to debt forgiveness that you may want to consider is debt consolidation. While this method doesn’t cancel the debt, it can help you pay it off faster and accrue fewer interest charges.

One of the most common debt consolidation methods is a balance transfer, which involves moving debt to a new credit card that offers 0% APR for a few months. During this time, you can work to pay off your debt without racking up interest.

Other options include taking out a personal loan or home equity loan to pay off your debt. The strategy here is that your new loan would have a lower rate than that of your current debt, allowing you to save on interest

Just be wary of for-profit companies that promise debt relief via consolidation, as they’re often pricey. Instead, look to nonprofits such as the National Foundation for Credit Counseling.

How to get debt forgiveness

If you’re moving forward with debt forgiveness, you have a few options depending on loan type and your overall personal and financial situation.

Federal programs

One of the few ways to get true debt forgiveness without consequences is to see if you’re eligible for a special program. Typically, these are only offered for student loan debt and home mortgages:

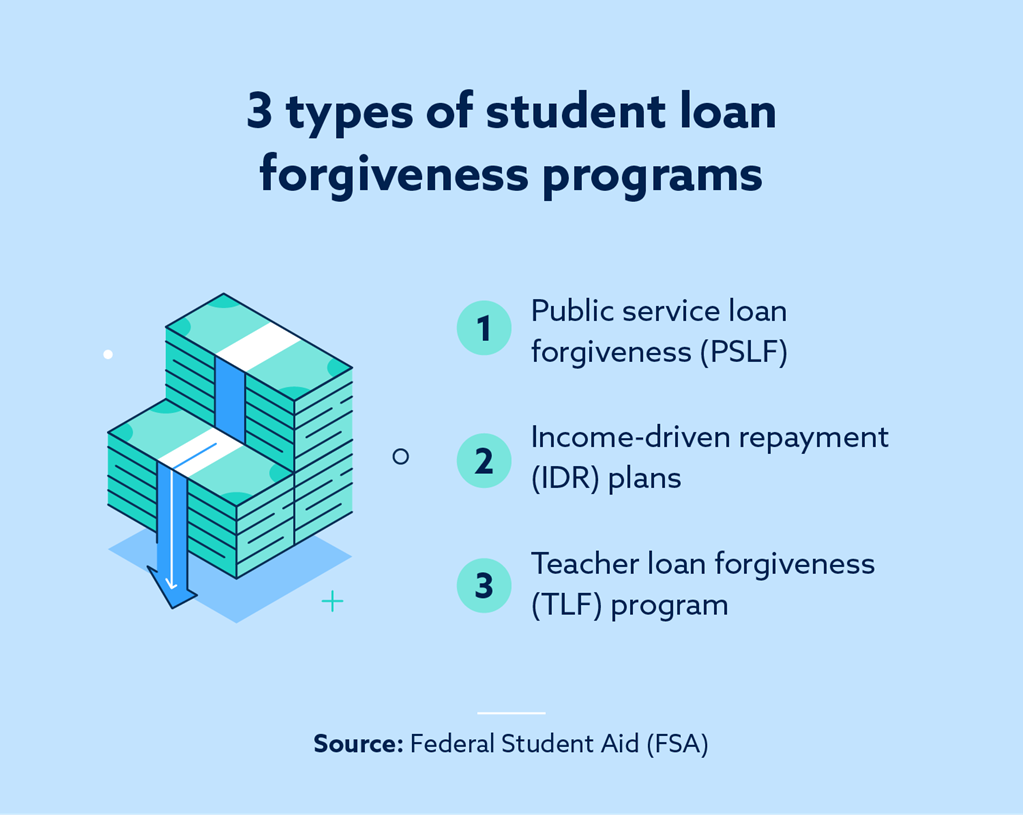

- Student loan forgiveness: In mid-2023, student loans totaled $1.7 trillion. To help alleviate this, the Public Service Loan Forgiveness (PSLF) program provides Direct Loan forgiveness for full-time workers of U.S.-based or non-profit organizations who have made 120 qualified monthly payments. Another type of student loan forgiveness is income-driven repayment plans, which forgive the remaining loan balance at the end of a repayment period. Thirdly, if you’re a teacher, you may be eligible for a Teacher Loan Forgiveness program.

- Mortgage debt forgiveness: The Mortgage Forgiveness and Debt Relief Act, enacted in 2007, lets eligible borrowers exclude up to two million dollars in forgiven mortgage debt from their taxable income. This allows forgiven mortgage debt and foreclosure balances to be truly penalty-free.

You may be eligible for other federal programs to help manage debt. To explore your options further, the Federal Trade Commission has guidelines for getting out of debt.

Settlement

Settlement is by far the most common form of debt forgiveness. It’s the process of negotiating your debt to only repay a portion of your outstanding balance. The rest is forgiven, meaning repayment is not necessary.

Borrowers tend to choose debt settlement if they can’t afford expensive and persistent debt payments. They may also choose this route as an alternative to declaring bankruptcy, since debt settlement should only stay on your credit report for seven years.

However, it’s important to watch out for hefty fees from these companies. If hiring a debt settlement agent is beyond your means, keep in mind that negotiating on your own is an option. First, you’ll need to determine your outstanding balance and what monthly payment you can afford. Next, contact your creditor. You’ll need to explain why you can no longer afford the loan and then negotiate a lump sum. If they agree, ask for a written letter so you have legal proof of the settlement.

Statute of limitations

If you’re seeking debt forgiveness for credit card debt, you may be able to leverage the statute of limitations (SOL) in your state. The SOL is applicable once a certain amount of time has passed (typically three to 15 years depending on what state you live in) and your debt collector hasn’t pursued debt collection in court. After this time frame, they have no legal claim to your money, and they should no longer be able to successfully sue you to collect the debt. However, this approach is risky for a number of reasons.

SOL start to accrue after the date of last activity, which includes payments and charges. After your SOL expires, a lawsuit can still be filed against you—but you can use the SOL as a defense in court.

Bankruptcy

Filing for bankruptcy is an option and that decision will remain on your credit report from seven to ten years. That said, it may help forgive some of your debt.

If you file for Chapter 7 bankruptcy, your debt is forgiven and some of your assets remain with you subject to certain state and federal exemptions.

If you file for Chapter 13 bankruptcy, you’re still required to pay off your debts. However, the court will assign you a payment plan spanning anywhere from three to five years, and they may reduce your outstanding balance to lessen the financial burden.

What are the consequences of debt forgiveness?

After you have a portion of your debt forgiven, you may feel like you’re out of the woods—and for the most part, that’s true. However, there are a few circumstances you’ll need to be aware of so that you’re prepared for the effects debt forgiveness may have on your finances.

Taxes

No matter which debt forgiveness route you take (with the exception of bankruptcy), you’ll likely end up with a higher taxable income. If the amount of forgiven debt exceeds $600, you’ll receive a 1099-C form titled “Cancellation of Debt” from the creditor.

With this form, you report the amount of your forgiven debt to the IRS and pay income tax on it. When you first take out a loan or borrow money, you’re not charged taxes on it because there’s the assumption that you’ll pay it back. But after debt forgiveness, that assumption no longer applies, which is why this essentially “free money” is now considered taxable income.

The upside is that the income tax you owe on the forgiven debt amount is less than what you would have to pay if you still owed the debt. Make sure to plan for this expense so that it doesn’t surprise you, especially if the forgiven amount is sizable.

Consider contacting a qualified tax professional for help accurately filing your taxes. Then, once you properly report your debt forgiveness to the IRS, you’ll want to check your credit report.

Credit score

The unfortunate reality is that debt forgiveness may negatively affect your credit score. Of course, there is no way to say for sure. What will improve is your debt to income ratio. The effect to which debt forgiveness impacts your credit largely depends on how you choose to seek debt forgiveness.

Bankruptcy can be the most devastating option for your credit score. According to Debt.org, a FICO score of 780 could take a 240-point dip, and a score of 680 could take a hit of 130 – 150 points. If your credit score is much lower than 680, you may not see as large of a dip. However, if you have no late payments or charge off on your credit report prior to filing bankruptcy, your score dip is far less.

Debt forgiveness provides a much-needed solution for borrowers struggling to make payments. However, it also comes with conditions. When considering which debt management plan is right for you, a little careful planning can go a long way.

If overwhelming debt has caused your credit to dip below where you’d like it to be, see if we could help. We can take a look at your credit report and assist you with moving forward.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.