The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

When done correctly, debt consolidation loans usually do not hurt your credit long-term.

When done correctly, debt consolidation loans usually do not hurt your credit long-term. In fact, there’s a good chance that they will ultimately improve your credit. However, debt consolidation can initially knock your score down a bit, which is why it’s important to do your due diligence before pursuing this strategy.

Debt consolidation is a way to combine multiple debts into a single loan. This not only reduces the interest you owe, but it also helps you organize your debt, making payments more manageable.

Debt consolidation can have positive and negative effects on your credit score. Here are a few areas it may negatively impact:

- Credit applications: Applying for a personal loan or a balance transfer card requires that a hard inquiry be performed on your credit. This will likely lower your score a bit initially as you get the consolidation process started.

- Average age of credit: The ages of your credit accounts matter, with older accounts garnering better credit scores. When you open a new account, it lowers your average credit age, which may initially negatively impact your score.

On the other hand, the following categories tend to be positively impacted by debt consolidation:

- Credit utilization: A new debt consolidation account will usually increase the amount of available credit you have. As long as you don’t begin spending significantly more after opening the new account, you’ll be using less of your available credit, which will benefit your score.

- Payment history: If you consistently pay off your new loan on time, your credit will likely be positively impacted.

Effects on credit score depend on the debt consolidation method

Each debt consolidation method comes with its own benefits and drawbacks. It’s important to acquaint yourself with the potential impacts of each method to make sure that consolidating debt results in a net gain for your credit health.

Balance transfer

A balance transfer is the process of transferring debt to a single credit card with a lower interest rate, allowing you to pay off your debts for less. Many balance transfer cards offer zero-percent APR during an introductory period, providing a window to pay off debt interest-free.

Despite the benefits offered, a balance transfer card could damage your credit score. First, applying for a new credit card may warrant a hard inquiry, which can bump your score down a bit. Second, your credit score is partially determined by credit utilization, and transferring significant amounts of money to a card and then paying it off involves high credit utilization on that card. This will likely harm your score.

If you decide to pursue a balance transfer card to pay off debt, be sure to investigate the card’s APR following the introductory period. Your interest rate may take you by surprise and skyrocket if you don’t do your due diligence.

Personal loan

Another popular debt consolidation method is taking out a personal line of credit. These loans are available at any time and can be used to quickly pay off debt.

If used correctly, personal loans can improve your credit score by diversifying your credit mix, especially if you’ve only had credit cards up until this point. Paying off debt with a loan rather than with credit can also reduce your credit utilization, which may boost your score.

That said, it’s important to remember that this process involves taking out a loan that must be paid back on time. You may also want to reconsider this option if your present score doesn’t allow you to take out a personal loan without being charged a high interest rate.

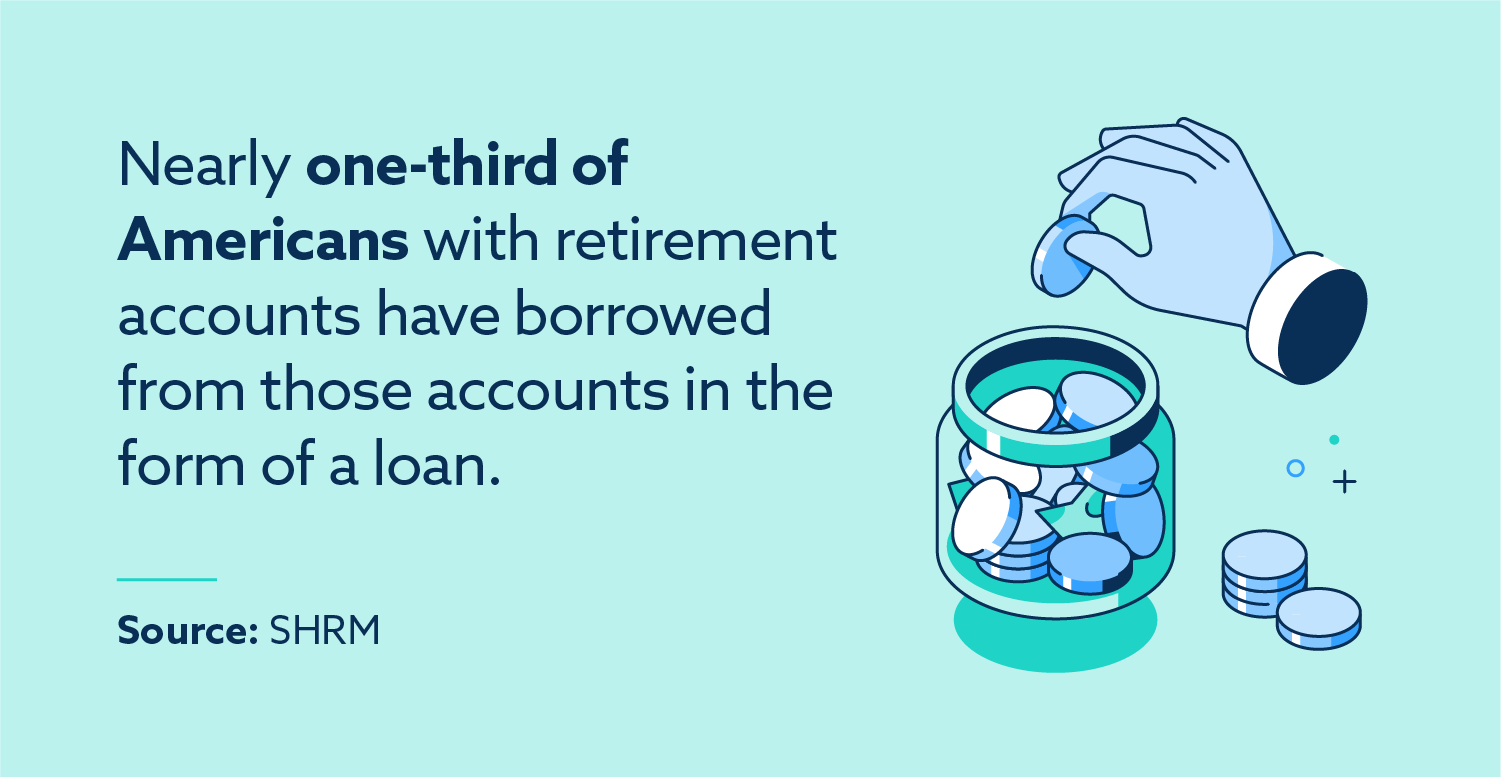

Borrowing from a 401(k)

If you have a 401(k) retirement account, you can borrow up to half of this balance to pay off debt. While it must be paid back within five years to avoid penalties, borrowing from a 401(k) does not have any adverse effects on your credit score. Moreover, the money you borrow doesn’t accumulate interest since 401(k) funds aren’t borrowed from a lender.

However, it’s important to remember what a 401(k) is meant for—retirement. Taking out funds for short-term debt payments can significantly detract from your retirement savings. You may also have to deal with tax repercussions when taking this course of action.

Home equity loan or line of credit

Home equity loans or lines of credit are perhaps the riskiest forms of debt consolidation, but they also offer some significant benefits. Essentially, lenders will offer you a loan and use your home as collateral. This means that if you fail to pay off the loan within the amount of time agreed upon, you could lose your home.

You must have excellent credit to take out a home equity loan or line of credit. When you apply, you will be hit with a credit check, which could initially lower your score a bit. While the impact on your score will likely be relatively insignificant, these loans can also accumulate very high interest, so it’s important to use discretion before taking one out to pay off debt.

Other options to consider

If debt consolidation doesn’t feel right for you, that’s okay. There are other debt relief options that could help restore your peace of mind regarding your financial situation.

Debt management program

Debt management services can help by counseling you regarding your options when you’re struggling with debt. A debt management program will likely involve a counselor negotiating lower interest with creditors and potentially closing credit cards.

While visiting a counselor at a debt management agency doesn’t harm your credit score at all, entering into a debt management program that reduces how much you have to pay does usually negatively impact your score. Your credit report will likely reflect the debt management program in effect until you are no longer using it.

Debt settlement or bankruptcy

Debt settlement is the process of negotiating with creditors to pay significantly less money than you owe to have your debt forgiven. Bankruptcy is a legal process that helps people organize and sometimes eliminate their debt. Bankruptcy, however, is a more long-term option than the other ones we’ve mentioned.

These two options should be a last resort when struggling to pay off debt, as they can have a significantly adverse effect on your credit score. Both debt settlement and bankruptcy will remain on your credit report for upwards of seven years, and sometimes up to ten years, negatively impacting your ability to open new accounts or apply for a loan. However, if you need to take care of massive debt now and you take wise financial steps in the future, these processes could end up ultimately being the right solution for you.

Should I consolidate my debt?

Before pursuing debt consolidation, it’s important to take a comprehensive look at the reasons you’re interested in consolidating debt and your plans for the foreseeable future.

Do you have a high interest rate?

If the interest on the debt you owe is 20 percent or more, you’ll likely save money by consolidating debt. However, certain balance transfer options charge fees that may counteract the benefits of debt consolidation. Do your research ahead of time to figure out which option saves you more money.

Are you missing payments?

Keeping track of all of your accounts can be stressful. If remembering to pay your bills has been a struggle and you’ve found yourself repeatedly missing payments, debt consolidation may help. Consolidating your debt could simplify your financial life by allowing you to take care of all payments at once. This will also benefit your credit in the long run, since missed and late payments can be detrimental to your score.

Do you need excellent credit in the short term?

If you’re planning to take out a loan or a mortgage anytime soon, you may feel the need to safeguard your credit score at all costs. Since many debt consolidation methods will put a temporary dent in your score, it may be wise to hold off until after you’ve been approved by a lender.

Ultimately, whether you decide to pursue debt consolidation and which method you choose depends on the weight of your debts and what would benefit your credit most. If you’re still on the fence, it’s a good idea to consult a financial advisor before making any decisions that could have long-lasting consequences.

Whichever decision you make, remember to keep your credit health at the forefront of your mind, and to take the steps where needed to repair your credit to expand your financial opportunities.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.